Canalys outlook: predictions for the technology industry

19 December 2024

Canalys is part of Informa PLC

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC’s registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

At the 2024 Canalys Channel Forum events in Berlin, Miami and Bali between October and December, Canalys analysts laid out their top predictions for the technology industry up to 2027. This is a rundown of 10 of those predictions:

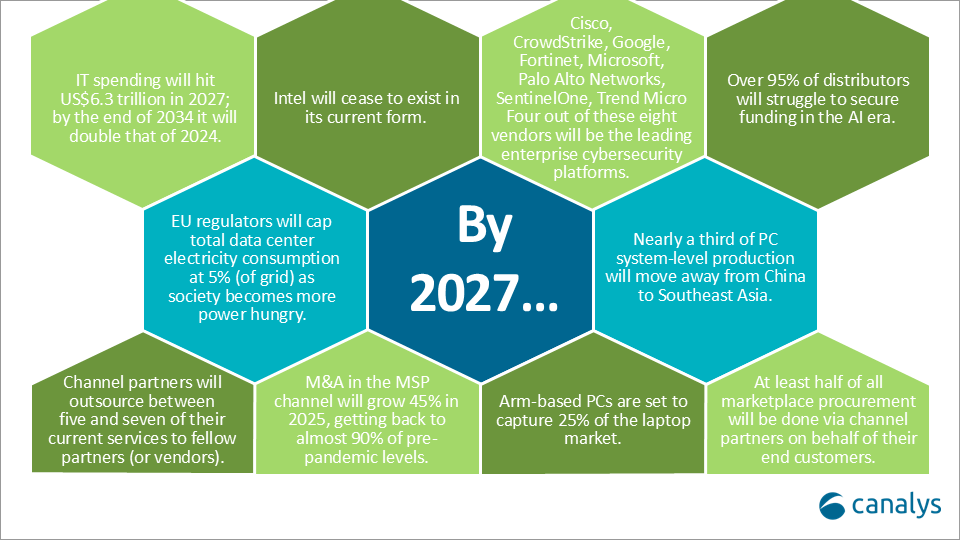

By 2027, the technology industry will be worth US$6.3 trillion. Growth in IT spending, across hardware, software and services will accelerate over the next three years, supercharged by AI. Investment in AI-powered software, cybersecurity and AI-capable PCs will drive robust growth, while the continued buildout of data centers to run AI by the hyperscaler cloud service providers will sustain growth in servers, storage and networking. The shift in focus from operational efficiencies to longer-term strategic challenges and embedding AI across all business functions will re-accelerate IT services growth, while managed IT services will remain a key growth engine for partners. Cloud infrastructure services will re-accelerate as customers focus on infrastructure modernization to capitalize on Generative AI.

Within the next 10 years, spending will have doubled from this year’s total to exceed US$10 trillion.

Intel hit the headlines in 2024 with poor financial results and over the US Thanksgiving weekend it was announced CEO Pat Gelsinger is retiring. In place are co-CEOs, David Zinsner and Michelle (MJ) Johnston Holthaus. Holthaus has been appointed CEO of Intel Products. Canalys expects Intel will separate its foundry business. The launch of the foundry business was a significant strategic shift, but it has been under significant pressure (as evidenced by the leadership change). The foundry unit had seen some important wins, especially with AWS, but it is yet to prove a real challenger to TSMC and Samsung. Foundry’s number one ally is the US government which is keen to ensure a local silicon industry thrives and is investing to make this a reality, however Intel’s key challenge is that major fabless chip companies have not come around to seeing Intel as a manufacturing partner they can trust, having been long-term competitors. A separation will help Foundry gain more clientele.

Consolidation has been predicted in cybersecurity for the last 20 years, but it has not yet materialized and, realistically, it will never happen. Cybersecurity always has significant M&A activity, but as threats continue to evolve, new cybersecurity vendors continue to proliferate. However, CISOs are inundated with tools and the need for consolidation is greater than ever. This does not mean one vendor platform will do everything, rather the winners will take an integration and partner first strategy with other vendors. The most successful platform vendors will be those that make partners a core component of their strategy, not just for transactional and more-service led channels, but also partners in adjacent sectors like insurance, financial services and marketing, and other cybersecurity vendors and ISVs that want to integrate and build value on top of the platform. This means vendors will need to expand their ecosystems and evolve their partner programs to reward partners at different stages of the customer journey, from influencing and landing the customer to expanding the account over time. The winning platform vendors will be those that can articulate and quantify the customer opportunity for partners with multipliers.

The pressure is increasing on distributors to deliver at a new level of scale, complexity and personalization, and to figure out the people, processes, programs and underlying technology that will drive competitive advantage in the platform economy.

They will face an increasing challenge as they seek funding. Distributors need to be able to build marketplace platforms (Canalys estimates that this requires over US$1 billion in investment) as well as come out of hiding and join their customer (the partner) in the seven trusted seats around the table. These actions will be necessary, but expensive.

GenAI is increasing the demands on the energy grid. In future, GenAI will account for 45% of data center electricity consumption, as well as the overall demand for power increasing. The rate of data center electricity consumption is already outpacing the grid’s ability to pump out more supply. Regulators, especially in the EU, will cap total data center electricity consumption at 5% to ensure that nation states can maintain critical infrastructure. Expect tensions with society to increase as demand for energy continues to rocket. Regulators may take a reactive approach if a real watershed or 'crisis' moment on this issue takes place before 2027. For example, widespread blackouts or a cut in water supply as data centers push grids and other utility infrastructures beyond their limits. It may take a high-profile story (as high-profile as the IT outage in July) for lawmakers to propose this kind of regulation.

By 2027, partner to partner relationships will expand as ‘Outsourcees become Outsourcers’. This will be ignited by greater compliance, security and data governance regulations prompting partners to co-partner with specialists. Sustained IT skills shortages (especially in cybersecurity, AI and sustainability) will result in partners leveraging the talent of their counterparts to expand their offerings. Vertical specialists will be in high demand by other partners that want to expand into other industries. Cost-savings and improved efficiency efforts will drive more GenAI usage and outsourcing of certain business operations.

Amid rising geopolitical tensions and the drive to prevent COVID-like supply chain disruptions, major PC vendors are actively working to diversify their manufacturing bases. In response to the stricter local manufacturing regulations in various countries, vendors are accelerating efforts to relocate system level production and expand final assembly operations outside China. By the end of 2027, Canalys forecasts over 50% of PC assembly – especially for the US-based PC vendors, and nearly one-third of system-level production – at the mother-board level, will be based outside China, with southeast Asia emerging as the new hub for these operations.

Despite efforts by Intel and AMD to strengthen the x86 platform through the newly formed advisory group, both companies will face increased competition from ARM-based processors. By 2027, one in four notebooks is forecast to feature ARM-based processors, driven by the presence of Qualcomm's X Series and Apple's M-series chips, with adoption further accelerated by the launch of NVIDIA's Grace CPUs. This shift will be driven by consumer demand, with a significant push from small and medium-sized enterprises, particularly in the Asia Pacific region. SMEs, which represent over 90% of businesses in the APAC region, are typically more flexible in their technology choices, supporting this shift to ARM-based solutions. For the channel, a wider range of silicon partners is a good thing – there will be more products to sell and more competition. However, it will require managing more complex PC portfolios and finding effective routes to market for products that still face skepticism in enterprise scenarios.

The growth in hyperscaler cloud marketplaces represents an important shift in customer procurement, but creates clear risks for the channel. One of the biggest fears is being cut out of the procurement process in the future. Enterprise customers continue to invest heavily in upfront, multi-year commitments with the major hyperscalers, in order to access discounts and in anticipation of increased cloud consumption to support AI workloads. But customers will be under greater pressure to show how they are leveraging these commitments. Greater macroeconomic pressures and increased board scrutiny are creating new challenges for business leaders. This makes the ability to use a proportion of these commits to purchase third party vendor SaaS products even more attractive. Partners will become an increasingly important access point for marketplace transactions as hyperscalers look towards channel offers to enable greater draw down of the cloud commits.

Managed services revenue growth will hit 13% in 2025 as outsourcing trends continue and end-customers look for more comprehensive risk management and cost optimization. But Canalys is also seeing more roll-up MSPs backed by private equity firms acquiring specialists. Those with AI, automation, and cybersecurity capabilities will be at the front of the pack, as these MSPs have made the investments that are most valuable to end-customers. Those with key certifications, such as CMMC or Cyber Essentials Plus, are also seeing the most brand recognition and will be among the most acquired.