Canalys outlook: predictions for the technology industry in 2024

02 January 2024

Canalys is part of Informa PLC

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC’s registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

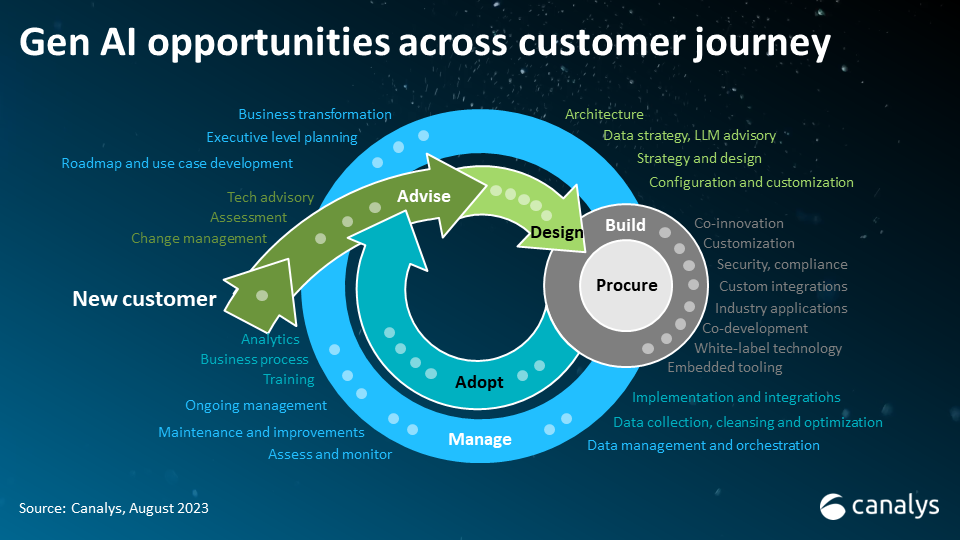

2023 presented new challenges for the technology industry. Inflation, rising interest rates and even war put pressure on the global economy, and particularly IT budgets. Despite this, the emergence of generative AI has been a paradigm shift that has shifted the emphasis of IT strategies and created a new and significant opportunity for the channel. The opportunities in generative AI are significant but are not the only ones that should provide the channel with optimism going into 2024 and beyond.

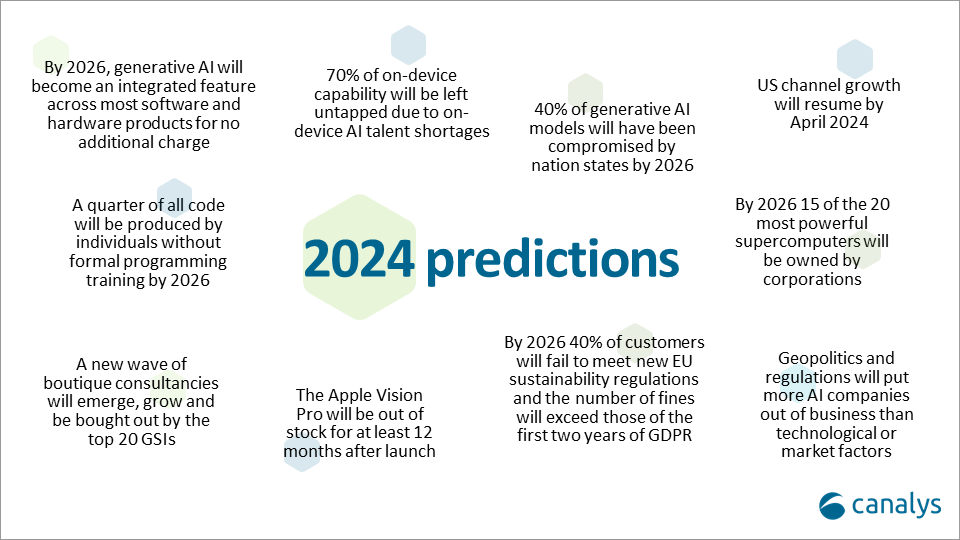

Generative AI remains early in its lifecycle, and while it is currently a multi-billion-dollar opportunity for the channel the opportunity will grow to US$158 billion by 2028. This revenue will mainly be realized in AI services and AI software development in the next 18 months and will be a critical part of continuing to embed generative AI across all industries and products. By 2026, the results of these efforts will be realized as most software and hardware products will feature an integrated or embedded generative AI feature. Most importantly, this will be a consumer expectation and so included at no additional charge. While in the early adopter stage, there are companies looking to charge for their generative AI offerings (Microsoft with Co-Pilot and Salesforce with Einstein GPT are just two examples), this will be an exception rather than a rule. To successfully capture the generative AI opportunity that exists and continues to grow, partners will need to co-innovate with vendors and customers alike to solve a fundamental challenge. These problems will continue to be service-led and partners will need to continue to provide those services for their customers. How do companies integrate these revolutionary but complex features in a way that is both solving business problems and profitable? That is the challenge to be overcome by the channel and could be the driver of future revenue for those companies that succeed.

2023 has been about the positive opportunity that exists because of the advances made in AI this year, especially around generative AI. Vendors have invested and will continue to invest in these technologies, and the progress in hardware will be monumental. This means that by 2025, dedicated AI chips performing over 100 TOPS will emerge. While the power of these will be significant, Canalys predicts that 70% of on-device AI performance will be left untapped, as talent deficiencies mean capabilities will not be properly optimized to the hardware potential. The talent shortages will be most acute in areas such as high-performance, low-power AI model optimization, on-device neural architecture search, and creating specialized AI inference chips and libraries tuned for edge devices. Major hardware makers have begun and will continue to stockpile talent to ensure their positions. Latecomers, such as Apple, have been aggressively hiring, hoping to take the lead in on-device AI to outpace their competitors. From a talent perspective, traditional software developers without on-device AI skills will struggle to remain relevant and fall behind. Avoiding this lag will require investment at a state level. Countries such as India and Indonesia that invest heavily in STEM education with their significant younger populations will mitigate some of the growing talent gap. As talent becomes increasingly more difficult to acquire, the time to prepare is now.

The productivity benefits of generative AI have been clear to see throughout 2023. But as these models become more complex and better trained, the cybersecurity threat is also important to consider. Enterprise organizations have been spending millions of dollars to build and train AI models in the hopes of transforming their businesses. From the moment ChatGPT was launched, many have been attempting to accelerate their development schedules and this focus on speed has expanded and will continue to expand available attack surfaces for threat actors. For nation states, the potential for espionage and disinformation and the ability to hold multinational firms to ransom will be the primary motives behind attacking these models. They will launch interference and poisoning attacks to access the sensitive training data that drives these models. With the trust in AI performance and output at stake, cybersecurity startups have emerged that will be able to provide real-time visibility into AI assets, to discover, validate and secure. The threat will be potentially huge, and the big question is how seriously will organizations take this, and how will they leverage the channel to protect themselves?

Despite initial challenges from the pandemic, there was unprecedented growth at the start of the 2020s. Growth in 2021 and 2022 was driven by cloud adoption, remote and then hybrid working, and the IT challenges and infrastructure required to support this. 2023 changed this significantly. The year saw two major wars, related energy price spikes and inflation. These issues have caused major challenges for technology companies and channel partners. Partners that are holding inventory, for example, are seeing this cost become increasingly more damaging to their bottom lines as this inventory loses value at a greater rate because of inflation. Consequently, 2023 saw a set of challenging results across the technology sector, including a 7% drop in growth for the US Channel Titans in the first half of 2023 and a 10% fall in Q3. In addition, interest rates have finally risen from their historically low levels for the first time in many years. This doesn’t just affect the venture capital and private equity firms that have been able to leverage these low rates to drive their success but also the start-ups and partners that have become overly reliant on this funding to maintain unprofitable growth. While cheap money made these actions virtually consequence-free, this is no longer the case. Those companies that have maintained their cash reserves are well protected, but those reliant (whether by choice or circumstance) on debt have seen challenges throughout the year. In 2023, there have been significant efficiencies, including several mass layoffs across the sector. Efficiency will remain the name of the game in 2024, and not just for channel partners, but also for vendors. Vendors across the spectrum, from Dell to Rapid7, have been adjusting their go-to-market strategies to be more channel-focused, as the channel is not just being seen as a revenue multiplier but a way of creating a more efficient go-to-market strategy. This, combined with improving conditions and early indications of growth from the Tech Titans (up 3% in Q3 2023), will mean that by April 2024, channel partners will collectively be seeing growth again and will have further embedded themselves as the key drivers of growth for vendors.

Despite layoffs throughout the year, certain areas still require specialized talent and can be very difficult to hire for. Coding and development is one such area that has, until recently, required deeply specialized training and investment from companies wishing to develop technology in-house. In 2024, according to a Canalys quick poll, 40% of channel partners plan to selectively recruit for their businesses, and this selective strategy is likely shared across the technology industry, with a focus on the recruitment of individuals who can code for many companies. One of the most obvious use cases and benefits of generative AI in its initial iterations has been the ability of AI models to write code. According to GitHub, around Copilot, users see around 40% of code generated by AI already, and this will only increase over time. As LLMs become more intuitive and individuals become more capable of understanding the correct prompts necessary to deliver functional code, a quarter of all code will be produced by individuals without formal programming training. AI will be responsible for launching the next wave of no-code building.

The wait for the necessary computing power, particularly in the public cloud, without investment from hyperscalers (and the necessary strings attached to these investments) to fuel the large language models that drive generative AI is at least two years. Beyond this, sustainability and security concerns that arise from the scaling of AI products and features further the level of complexity that businesses face when adding AI to their overall digital strategies. All of these risks emerge, even while businesses still face the challenge of how to actually generate efficiencies and value from the use of generative AI. While the amount of spend coming out of the line of business within organizations surpasses that of the spend out of CIO offices, the ability for end-customer stakeholders to fully understand and, therefore, leverage the benefits is dependent on the partners they choose to work with. As discussed in our report on generative AI earlier in the year, there was a US$15.8 billion opportunity tied to generative AI in 2023 that will grow to US$158 billion by 2028. Most of this opportunity, particularly in the first 18 months, will be a services opportunity that will rely on solving specific problems that rely on hyper-personalized and hyper-specialized solutions. While this specificity will be challenging, the market opportunity is significant. For many leaders in the channel, this clear market opportunity, combined with the five-year CAGR in generative AI of 59.3%, will be too tempting. Many will exit their current companies to start boutique AI consultancies. The most successful of these consultancies will grow to see multiple millions in revenue with employee counts up to 20, which will lead to the inevitable – being acquired by a global systems integrator. These GSIs, while already investing multiple billions in their own generative AI services practices, often expand into new areas of expertise (particularly when it comes to more specialized offerings) by simply acquiring boutique competitors in the area, and the emergence of these new boutiques will create a new type of acquisition target for these top GSIs.

With the failure of Google Glass and Meta Quest to capture the popular imagination, there is clear proof that, once again, being first to market does not guarantee success. Vendors must first understand the customer use case and what is driving demand before committing to a product category. As has been the case in previous years, the vendor that has managed this more than most in the hardware space has been Apple. By redefining the XR category, with a focus on making a functional computing experience rather than AR or VR, Apple is focusing on consumer experience and utility, over-engineering features such as immersion levels, thin design and lack of controllers. Its high price point (starting at US$3,499) will mean financial success. Apple will be relying on the Vision Pro to break its mold of key products (iPhone, iPad and Mac) to show it can continue to lead in the innovation category. While Apple will continue to rely on its own strong ecosystem of first-party applications and content, the channel will also be looking to support the expansion of this new product. In a recent Canalys quick poll, 54.4% of respondents who resold Apple products intend to resell the Vision Pro headset next year, with this number likely increasing as the use cases expand with product maturity. With this level of commitment and demand, it is likely that demand for the Vision Pro will cause it to be out of stock for many for at least 12 months after release, potentially even longer.

According to the Canalys Global ESG Regulation Tracker, there are over 100 sustainability regulations globally to contend with for end customers. This regulatory landscape is only becoming more complex as states look to manage the impact of the global economy on the environment. This challenge in the technology industry is becoming even more stark with the impact that AI (generative and otherwise) will have in terms of its demands on infrastructure. The water-intensiveness of complex AI models, combined with the e-waste from upgrades needed to infrastructure to handle the new models needed for AI, will be a challenge. As CSRD reporting requirements loom, customers will need support to meet these reporting requirements. This will act as a catalyst for IT spending, as part of the US$247 billion market opportunity that exists in sustainable IT. This is mostly going to be in the form of energy optimization, circular IT and consulting and advisory services. 15% to 20% of revenue for partners will likely be in sustainability services as customers look to avoid falling into the 40% of businesses that fail to meet their sustainability regulatory obligations. Vendors will need to step up their preparations as well, though, as only 16% of partners receive sustainability resources and support from all the vendors that they work with. In contrast, 40% of partners receive this support from only a few or none of their vendors, which will be a significant driver behind the fines faced by customers by 2026.

2023 saw the acceleration of the race for computing power. Today, only six of the top 20 of the most powerful supercomputers are currently owned by corporations, but Canalys predicts that in the next two years, the balance of power will shift, and by 2026, 75%, or 15 of the top 20 most powerful supercomputers will be privately owned and operated by corporations. This would be a significant shift in the ownership of compute power from public to private and indicative of the shift of power and influence within the geopolitical and economic landscape. This shift is being driven by an AI arms race that exists not simply in the technology sector, but across every industry. Enterprises are building massive AI systems to transform their businesses, but there are long lead times and a dependence on a small pool of technology leaders to meet the demands for compute power that stand as the basic foundation of the AI revolution. Nvidia expects that by the end of 2023, it will have shipped over 500,000 H100s, but the majority of these have been purchased by the hyperscalers. Furthermore, according to Pitchbook, two thirds of the US$27 billion raised by AI start-ups in 2023 was provided by Amazon, Google and Microsoft, significantly out-funding VCs and private equity firms, indicating how much of a priority AI has become for these firms. Beyond the hyperscalers, firms such as Tesla have invested heavily, with the peak performance of their latest supercomputer, using over 10,000 Nvidia H100 GPUs, likely becoming the fourth most powerful system in the world.

As with any emerging technology, market forces and technological limitations will always be a challenge to navigate for new companies trying to find a niche that will be profitable and meet market demand. But the extent and potential danger of AI will necessarily involve and interest nation states and regulatory bodies in a more significant way. AI is likely to become the next sphere in which nation states compete for control and, ultimately, supremacy. Politicians will look to slow the progress of the private sector through regulation (efforts such as the 2023 AI Safety Summit show the intent of politicians already) to not only allow their own public efforts to catch up but insist on greater security. Ultimately, governments will look to leverage their influence to restrict data access, impose trade barriers and even go as far as banning certain technologies. Data restrictions will be influential as, without the necessary data, companies will not be able to build and train their AI tools to the necessary standard to create utility. Limits in trade will also present challenges of scaling across both geographies and user bases.